Block: Beyond the Counter

How Block is Weaponizing ‘Wallet Media’ to Invent the Next Era of Commerce

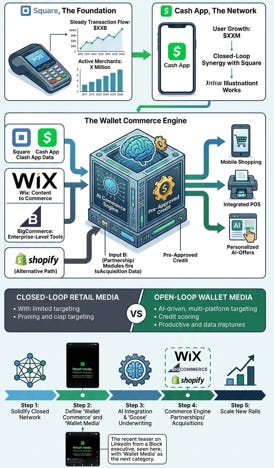

When Sach Malik, Cash App’s Global Head of Revenue Strategy and Operations, recently teased a simple graphic on LinkedIn with the words ~~*Retail media*~~ replaced by **Wallet media**, the market viewed it as an intriguing ad campaign ahead of Cannes Lions. In reality, it was a declaration of a fundamental paradigm shift. Block is not just adapting to the era of artificial intelligence; it is inventing a new market category—**Wallet Commerce**—and potentially dismantling its own closed loops to orchestrate it.

For the past decade, financial analysts characterized Block (formerly Square) by its two distinct, multi-billion-dollar closed ecosystems. On one side stood Square: an ecosystem serving millions of brick-and-mortar merchants with point-of-sale hardware and back-office software. On the other stood Cash App: a hyper-engaged consumer application serving over 50 million active users. The overarching strategy was clear—link the two via payment rails, discovery, consumer finance, and build an impregnable double-sided moat.

However, the limit of a closed network is its boundaries. In an economic landscape disrupted by intelligent AI agents and real-time data layer interoperability, maintaining strict walls around an ecosystem restricts growth. Block’s latest operational movements signify a massive structural evolution: potentially transitioning from a powerful closed loop to an **Open Commerce Engine** powered by artificial intelligence and supercharged by proprietary credit underwriting.

### The Evolution of a Paradigm: From Retail Media to Wallet Media

To understand “Wallet Media,” one must first observe the massive boom of Retail Media Networks (RMNs) pioneered by giants like Amazon, Walmart, and Target. Retail media allowed brands to buy ad space directly at the digital point of sale, leveraging first-party transaction data to target consumers when their intent to buy was highest.

But traditional retail media possesses a fatal flaw: it is tethered to the retailer’s physical or digital storefront. A Walmart ad network can capture your preferences when you shop at Walmart, but it cannot follow you into a local boutique, a digital independent store, or your peer-to-peer transaction history.

**Wallet Media** shatters this constraint. Because the digital wallet lives in the user’s pocket across every facet of their daily life, its data capture is universal. It understands peer-to-peer liquidity, investment appetites, bitcoin purchases, localized offline spending via the Cash App Card, and digital checkout preferences. The wallet knows what offers and promotions a user engages with and what credit incentives are needed to encourage a sale. By rebranding this intersection as Wallet Media, Block is asserting that the modern ad network is no longer a destination; it is the financial interface itself.

Retail media occurs inside a store. Wallet media occurs inside the human financial workflow. By moving the context of commerce from where products live to where capital lives, Block changes who controls consumer demand.

### Dismantling the Closed Loop: Engineering the Open Network

Historically, Block’s plan was closed-loop integration: keeping Square transactions routed directly into Cash App balances. Yet, to maximize the true potential of Wallet Media, Block must pivot toward an open distribution strategy. The goal is to deploy an omnipresent **AI Commerce Engine** capable of ingesting data from any point of sale and presenting optimized purchasing offers directly to consumers via Cash App.

This strategy cannot rely on Square merchants alone. To scale rapidly, Block must transform into the universal transactional middleware for the internet. This is where strategic partnerships or outright acquisitions of enterprise-grade e-commerce platforms—such as **Wix, BigCommerce, or Squarespace**—become highly probable tactical moves.

Imagine Block giving access for Wix or BigCommerce merchants to 59 million Cash App users. A merchant on Wix can pair a 10% discount with 0% BNPL and measure the uplift. This allows Block’s consumer-facing AI engine to index inventory, track product metadata, and analyze pricing patterns across the global independent web.

### The AI Commerce Engine & The Credit Multiplier

With an open network feeding transaction data into Block’s database, the company’s AI capabilities can be fully realized. Block utilizes internal AI frameworks to execute synchronous processing of both consumer liquidity and merchant inventory.

The AI Commerce Engine does not merely recommend items based on a user’s past browsing history; it matches real-time consumer purchasing capability with merchant supply demands. If a consumer’s account shows a pattern of high-affinity clothing purchases, and a BigCommerce merchant has surplus inventory of an item in that exact size, Block’s AI bridges the gap dynamically.

The ultimate catalyst of this engine, however, is **proprietary credit**. Consumer data and merchant discovery mean very little if capital is friction-filled at the exact moment of intent. By leveraging the programmatic credit infrastructure of Afterpay alongside their internal credit profiling systems, Block can provide micro-targeted, pre-approved credit lines right at the digital storefront interface.

Because Block evaluates both the merchant’s real-time operational health and the consumer’s granular spending habits, its underwriting model achieves a significant predictive advantage over traditional credit institutions. The underwriting formula can be simplified conceptually:

Where risk is dynamically calculated as a function of real-time consumer liquidity streams, aggregate merchant sales velocity across the open platform, and AI-derived purchase affinity coefficients. This allows Block to confidently issue short-term capital where traditional credit scoring models see unmanageable risk, turning credit into a primary tool for driving user engagement.

### Conclusion: The Structural Edge of Distribution

The market frequently worries that foundational artificial intelligence models will commoditize fintech by making basic code, payment processing, and customer support incredibly cheap. While that commoditization occurs at the lower layers of the tech stack, it simultaneously increases the strategic value of consumer distribution and proprietary data sets.

By leveraging their massive scale to transition from an isolated dual-network architecture into an open, AI-driven wallet media infrastructure, Block is insulating its business from commoditization. They are defining the rules of a brand-new economic category: one where the digital wallet is no longer a passive repository for digital currency, but an active, intelligent orchestrator of global commerce.